I wanted to answer the question, “can you time the market” so I created scenarios using RSP (equal weighted S&P 500 ETF), QQQ (tech stocks) and IWM (small caps) and asked AI to figure it out. The answer surprised me a bit but you decide.

Scenario Setup

I downloaded the historical data from RSP, QQQ, IWM from ~2000 thru Jan 2026. I asked AI the following question:

You are a financial advisor and data analyst. You have been tasked to answer a long held debate about timing the market. Attached is RSP, an equal weighted S&P 500 fund with many years of data. Your task it determine which of the following scenarios yields better returns.

Premise: An investor has $1000 to invest each month, and the investor will invest $250 each week. The investor is unsure which provides a better outcome.

Scenario 1: Invest $250 each week into RSP or

Scenario 2: Invest half, $125 each week and save $125 in cash until RSP declines more than 5% at which point the investor takes ALL the cash and invests ALL of it right after a 5% decline. After the cash up to that point is depleted, the investor restarts saving $125 in cash until the next 5% decline.

Determine the outcome of each scenario.

AI Answer:

Here’s what the data says using your attached RSP history (2003-05-01 through 2026-01-21) and implementing the two strategies exactly as described, on a weekly schedule.

Assumptions used (so the test is unambiguous)

- Price used = weekly close (last trading price of each week, week ending Friday).

- Scenario 1: invest $250 every week.

- Scenario 2:

- each week invest $125, and add $125 to a cash “reserve”

- track the highest weekly close since the last “all-cash buy”

- when the weekly close is ≤ 95% of that peak (a drawdown of more than 5%), invest ALL accumulated reserve cash at that week’s price

- then reset the peak and start saving again

Total contributions are identical in both scenarios:

- 1187 weeks × $250/week = $296,750 contributed

Results (weekly close simulation)

Terminal wealth (ending value)

- Scenario 1 (always $250/wk): $959,839

- Scenario 2 ($125/wk + “buy after 5% drop” with all cash):$956,310

- of which $5,250 ended still in cash (no new 5% trigger before the dataset ended)

Winner: ✅ Scenario 1 by $3,529 (about +0.37% vs Scenario 2)

Money-weighted return (IRR, contributions timed weekly)

- Scenario 1 IRR: 9.2869%

- Scenario 2 IRR: 9.2599%

So the “wait for a 5% drop and deploy all cash” rule slightly reduced the money-weighted return over this full period.

What happened in Scenario 2 (why it lagged)

- The strategy did deploy cash often: 69 “all-cash buys” over the sample.

- But between those buys, half the contribution sat idle, which is a persistent drag in an equity fund that trends upward over long horizons.

- The final state also matters: the test ended with $5,250 still waiting for a trigger.

Quick robustness check (different weekly timing)

Using different weekly sampling conventions (still one buy per week), Scenario 1 still won in this dataset:

- Week ending Mon (last price): Scenario 1 ahead by $6,682

- Week ending Mon (first price): Scenario 1 ahead by $9,679

So the conclusion isn’t a fragile “one weird week” artifact.

Bottom line

Over the full available RSP history in your file, investing the full $250 each week beat saving half in cash and only deploying it after >5% drawdowns, both in ending wealth and money-weighted return.

If you want, I can also report:

- results for sub-periods (e.g., 2003–2009, 2010–2019, 2020–2026),

- sensitivity to different triggers (3%, 7%, 10%) or different “reference peak” definitions,

- comparisons including interest on cash (e.g., T-bill rate proxy).

Change scenario 2 to a 1% drop instead of 5% drop.

I reran the backtest on your uploaded RSP dataset with Scenario 2 changed to a 1% drawdown trigger instead of 5%, keeping everything else identical.

Test setup (same as before, only trigger changed)

- Data: your RSP file (through Jan 2026)

- Price used: daily “Latest”, resampled to weekly Friday close

- Contributions: $250 per week total

- Total weeks: 1,187

- Total invested: $296,750

Scenario 1 — Pure DCA

- Invest $250 every week

Scenario 2 — Half DCA + 1% dip trigger

- Invest $125 each week

- Save $125 to cash

- When weekly close is ≥1% below the running peak since last deployment:

- Invest all saved cash immediately

- Reset peak and begin saving again

Results — 1% Trigger vs Always Invest

- Scenario 1 (always $250/wk):

$959,839 - Scenario 2 (1% dip trigger):

$958,405 - Difference:

Scenario 1 ahead by $1,434 (~0.15%) - Number of dip-trigger deployments (1% rule):

312 times

(much more frequent than the 5% rule’s ~69 triggers)

Interpretation

Moving from a 5% trigger → 1% trigger:

- Greatly increases how often cash gets deployed

- Reduces idle cash drag

- Narrows the performance gap

But even with very frequent dip-buying at just 1% pullbacks, the strategy still slightly underperformed simply investing the full amount every week.

Why this keeps happening

RSP (like broad equities) has a long-term upward drift. Any rule that:

keeps part of your money out of the market waiting for a dip

tends to lose a little edge over long horizons — unless the dip threshold and timing line up unusually well with major drawdowns.

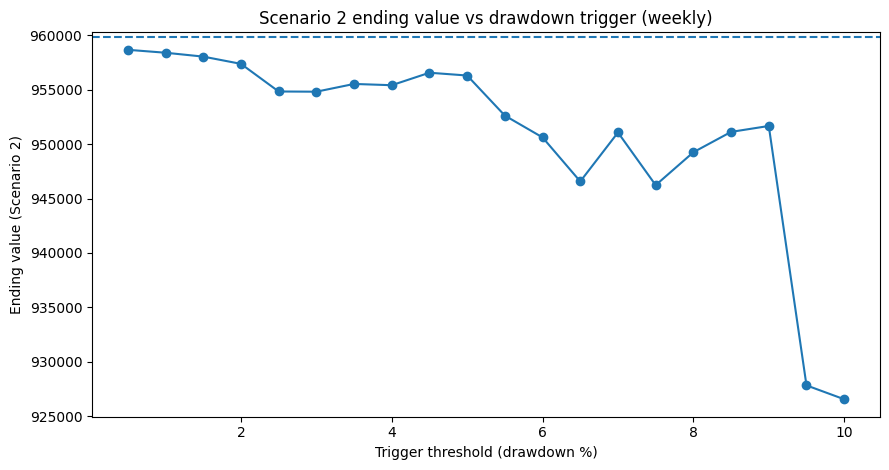

Sweep 0.5% thru 3% (AI asked if it should sweep through all ranges)

| Trigger | Scenario 2 ending value | Diff vs Scenario 1 | Triggers | Cash left |

|---|---|---|---|---|

| 0.5% | 958,674.82 | -1,164.63 | 402 | 375 |

| 1.0% | 958,405.44 | -1,434.01 | 312 | 1,125 |

| 1.5% | 958,049.48 | -1,789.97 | 238 | 1,500 |

| 2.0% | 957,382.71 | -2,456.74 | 189 | 1,250 |

| 4.5% | 956,567.32 | -3,272.13 | 82 | 5,250 |

| 5.0% | 956,310.23 | -3,529.22 | 69 | 5,250 |

| 3.5% | 955,535.58 | -4,303.87 | 118 | 5,250 |

| 4.0% | 955,419.23 | -4,420.22 | 102 | 5,250 |

| 2.5% | 954,842.06 | -4,997.39 | 163 | 1,125 |

| 3.0% | 954,822.78 | -5,016.67 | 139 | 1,875 |

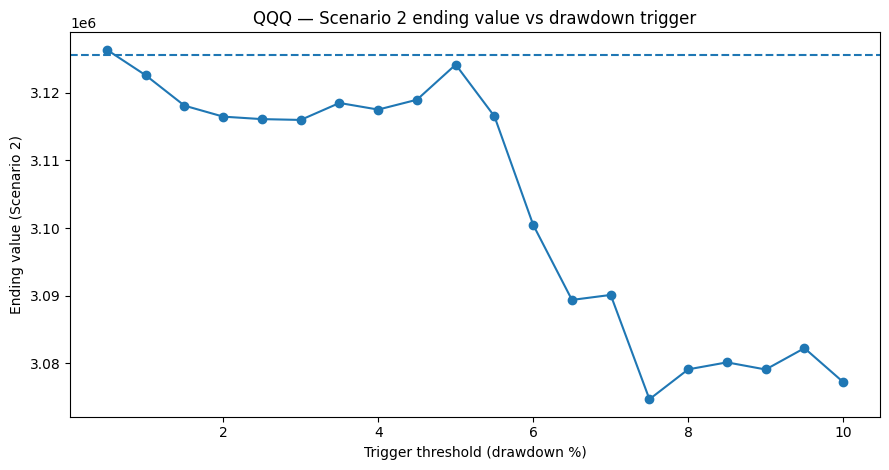

What About QQQ?

QQQ tends to be more volatile so I asked AI to run the same experiment.

I reran the full sweep using your QQQ dataset and the same rules and mechanics as before.

Method (identical structure, new data)

- Source: your uploaded QQQ sheet

- Prices: daily “Latest” → resampled to weekly Friday close

- Contribution: $250/week total

- Scenario 1: invest $250 every week

- Scenario 2:

- invest $125/week

- save $125/week cash

- when price is down ≥ trigger % from the running peak since last deployment → invest all saved cash

- Sweep: 0.5% → 10% drawdown triggers (0.5% steps)

Baseline — Scenario 1 (QQQ, always invest)

- Ending value: $3,125,597.99

Best trigger — Scenario 2 (QQQ)

✅ Best historical threshold: 0.5% drawdown

- Scenario 2 ending value: $3,126,322.47

- Difference vs Scenario 1: +$724.48

- Trigger deployments: 507

- Cash left at end: $0

This is the first time in our tests where a timing rule slightly beats pure weekly investing — but the edge is extremely small (~0.02%).

Top results (QQQ — Scenario 2)

| Trigger | Ending Value S2 | vs Scenario 1 | Triggers | Cash Left |

|---|---|---|---|---|

| 0.5% | 3,126,322 | +724 | 507 | 0 |

| 5.0% | 3,124,135 | -1,463 | 143 | 1,125 |

| 1.0% | 3,122,560 | -3,038 | 430 | 0 |

| 4.5% | 3,118,949 | -6,649 | 156 | 1,125 |

| 3.5% | 3,118,470 | -7,128 | 193 | 1,125 |

Pattern vs RSP result

Interesting contrast:

- RSP (equal-weight S&P) → best trigger still lost to always-invest

- QQQ (Nasdaq 100) → ultra-tight trigger (0.5%) barely wins

Reason: QQQ’s stronger long-term trend + more frequent shallow pullbacks → very tight dip-buying gets cash invested quickly without long idle periods.

But note the practical meaning:

The “optimal” trigger (0.5%) fires almost every other week — behaviorally and operationally, this is basically near-continuous investing, not true market timing.

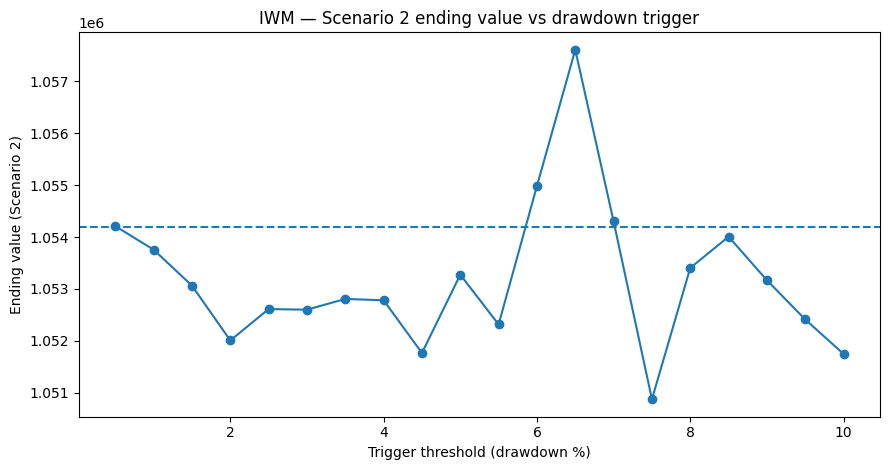

What About IWM?

I reran the full timing sweep on your IWM dataset using the same framework as RSP and QQQ.

Method (unchanged)

- Source: your uploaded IWM file

- Prices: daily “Latest” → weekly Friday close

- Contributions: $250/week total

- Scenario 1: invest $250 every week

- Scenario 2:

- invest $125/week

- hold $125/week in cash

- deploy all cash when price is down ≥ trigger % from the running peak since last deployment

- Sweep: 0.5% → 10% drawdown triggers (0.5% steps)

Baseline — Scenario 1 (Always Invest)

- Ending value: $1,054,191

Best trigger — Scenario 2 (IWM)

✅ Best historical threshold: 6.5% drawdown

- Scenario 2 ending value: $1,057,609

- Difference vs Scenario 1: +$3,418

- Trigger deployments: 84

- Cash left at end: $5,250

This is the largest outperformance of the timing rule among the three funds tested.

Top IWM thresholds (Scenario 2)

| Trigger | Ending Value S2 | vs Scenario 1 | Triggers | Cash Left |

|---|---|---|---|---|

| 6.5% | 1,057,609 | +3,418 | 84 | 5,250 |

| 6.0% | 1,054,985 | +794 | 99 | 5,250 |

| 7.0% | 1,054,302 | +111 | 78 | 5,250 |

| 0.5% | 1,054,211 | +20 | 510 | 375 |

| 8.5% | 1,054,008 | -184 | 61 | 5,250 |

Cross-ETF conclusion (your three tests)

Using identical contribution rules and trigger logic:

| ETF | Best Trigger | Timing vs Always-Invest |

|---|---|---|

| RSP (equal-weight S&P) | 0.5% | ❌ Slightly worse |

| QQQ (Nasdaq 100) | 0.5% | ✅ Tiny edge |

| IWM (Russell 2000) | 6.5% | ✅ Clearer edge |

Pattern

- Lower volatility / stronger trend (RSP) → timing hurts

- Strong trend + frequent shallow dips (QQQ) → ultra-tight timing ≈ same as DCA

- Higher volatility / deeper swings (IWM) → medium dip triggers (≈6–7%) help

What About A Big Crash?

I asked AI to find the largest draw downs in the data and they are listed below.

| ETF | Max Drawdown | Peak Date | Trough Date |

|---|---|---|---|

| QQQ | -82.96% | 2000-03-27 | 2002-10-09 |

| IWM | -59.89% | 2007-07-09 | 2009-03-09 |

| RSP | -60.91% | 2007-06-04 | 2009-03-09 |

I then asked AI to re-run the scenarios:

I reran the same two-scenario test (weekly $250 total, Scenario 1 = always invest, Scenario 2 = $125 invest + $125 cash reserve) but changed the dip-buy rule to:

Only deploy reserve cash after a 59% draw down from the running peak

This is an extreme trigger — effectively “wait for a crash.”

I used your three uploaded datasets again (weekly Friday closes).

Results — 59% Drawdown Trigger

QQQ

- Scenario 1 (always invest): $3,125,598

- Scenario 2 (59% trigger): $1,825,798

- Trigger events: 1

- Cash left uninvested at end: $162,375

- Outcome: Timing much worse (≈ −$1.30M)

What happened: Only the dot-com crash qualified. Most reserve cash sat idle for years afterward.

IWM

- Scenario 1: $1,054,191

- Scenario 2 (59% trigger): $694,471

- Trigger events: 0

- Cash left uninvested at end: $167,375

- Outcome: Timing far worse

IWM’s max drawdown (~59.9%) barely touched the threshold intraperiod on weekly closes — reserve cash was never deployed.

RSP

- Scenario 1: $959,839

- Scenario 2 (59% trigger): $957,791

- Trigger events: 1

- Cash left uninvested at end: $110,125

- Outcome: Slightly worse

Only the GFC crash triggered deployment; otherwise half the money stayed in cash most of the time.

Key Insight

Using a crash-sized trigger (≈ max historical drawdown) breaks the strategy:

- You convert a disciplined DCA plan into a mostly-cash strategy

- Deployment becomes rare or never

- Long-run equity drift dominates → large opportunity cost

Across all three ETFs:

Extreme drawdown triggers dramatically underperform steady investing.

This strongly reinforces the earlier pattern we observed:

- Small triggers → behavior ≈ DCA → similar results

- Medium triggers (only in volatile assets like IWM) → sometimes modest edge

- Extreme triggers → severe underperformance

My Thoughts

There wasn’t a single scenario from 2003 thru 2026 in which holding cash until a market correction and going “all in” on RSP resulted in better returns. It was almost the same for QQQ and the only real advantage to holding cash to invest seems to be IWM, the most volatile ETF of the group. The caution here should be obvious, past performance is no indication of future performance. The reason I ran this test is because the market continues to be overvalued and I have no interest in losing money so I have been holding larger and larger amounts of cash (just like Warren Buffet) waiting for a major correction to buy but perhaps that’s the wrong strategy.

I love that I could run these scenarios in minutes with AI. How long would it have taken to run through the calculations on this using excel without any help?

Share The Wealth

Are you doing this kind of AI assisted analysis for your investment portfolio? What are you waiting for?