Taxes are the bane of my existence and one of my pet projects is to use AI and build a tax optimization tool to lower or eliminate most of my taxes. As a starting point, I asked google’s gemini to build me a spreadsheet as a starting point. The first thing I wanted to do was model the tax implication and impact of dividend investments on three main different tax treatments: 1256 Contracts, Return of Capital, and ordinary income.

AI did a good job of building it out and I’m testing it and playing with it but have some screen shots below to illustrate the real issue I have with taxes.

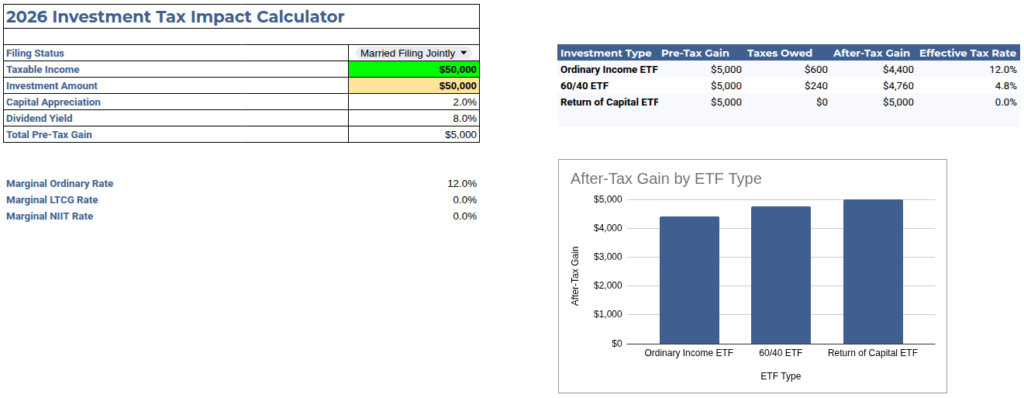

$50K Salary / $50K Dividend Investment

My first real salaried job was making about $50k per year back in the 90s. It was a good salary back then because I recall a family member was a teacher and was getting paid about half that amount. I did not have $50k in dividend investments back then either but the point here is to illustrate the tax impact.

The setup below is simple. The green box has taxable income presumably from a W-2 type job The investment amount is how much a dividend paying investment like JEPQ paying 8% and appreciating 2% would produce in income and how it will be taxed.

In the scenario below the tax rates are fairly low but there is still a sizeable difference between how ordinary income is taxed against a 60/40 1259 investment like SPYI. The Return of Capital has the lowest tax rate (for now, taxed later) but the 1259 ETF only has $240 in taxes.

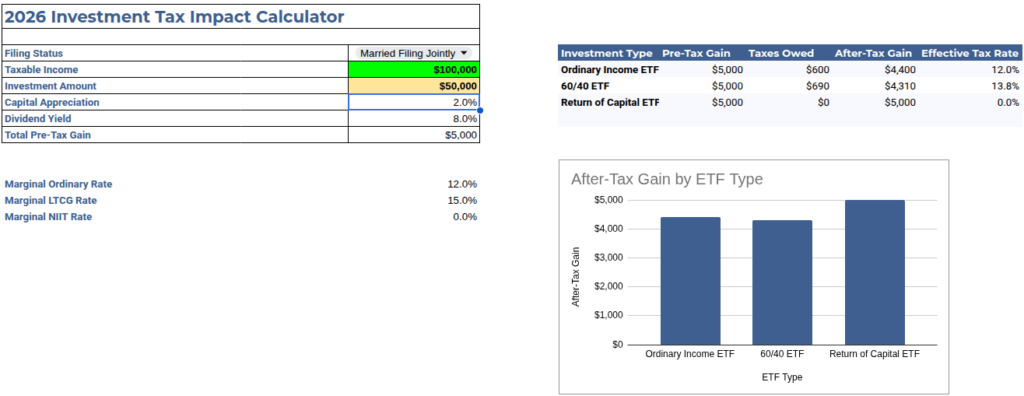

$100K Salary / $50K Dividend Investment

Now if we bump up the salary to $100k and leave the investment at $50k, the 1259 contract ETFs now have higher taxes than ordinary income tax! The tax rate is higher too.

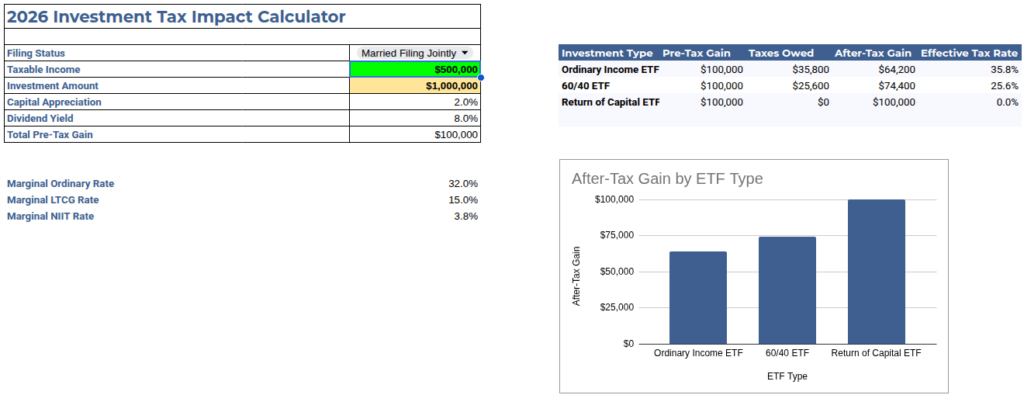

$500K Salary / $1M Dividend Investment

Now if you really bump up the income to $500,000 and an investment of $1,000,000, the tax rates between ordinary income and 1259 contracts changes dramatically. It’s a whopping 10.2% difference just because you chose a different investment. The mistake can easily cost $10,200 in this example. The higher the income and investments amount grow, the higher the tax bill unless it is optimized. I have already written about how I use municipal bonds to avoid taxation on interest in taxable accounts.

The Return of Capital tax rate is zero on all the variables here but there is no free lunch, the ROC has taxes on the capital gains after the investment has consumed all the initial capital and everything after that is taxes at the capital gain tax rate. The dilemma there is you have no idea what the capital gains tax rate will be in 10 years so while it may be a great deal now, it may be a worse deal later. An investor would need to keep an eye on tax law changes and decide to exit early if long term capital gain tax rates go higher in the future.

This is all just a starting point to conceptually build a calculator that optimizes my entire financial ecosystem that includes bonds, real estate, stocks, foreign currencies, precious metals, and other instruments. I don’t mind putting in the time because when I’m done, it will be 100% customized for my financial situation. This will be a journey as tax laws change every year but I am eager to get my taxes down as much as possible.

If you want a more detailed explanation of these concepts, Permission to Be Wealthy had a great video that goes into the details.

Share The Wealth

Are you having google gemini build your own tax system customized to your financial situation yet?