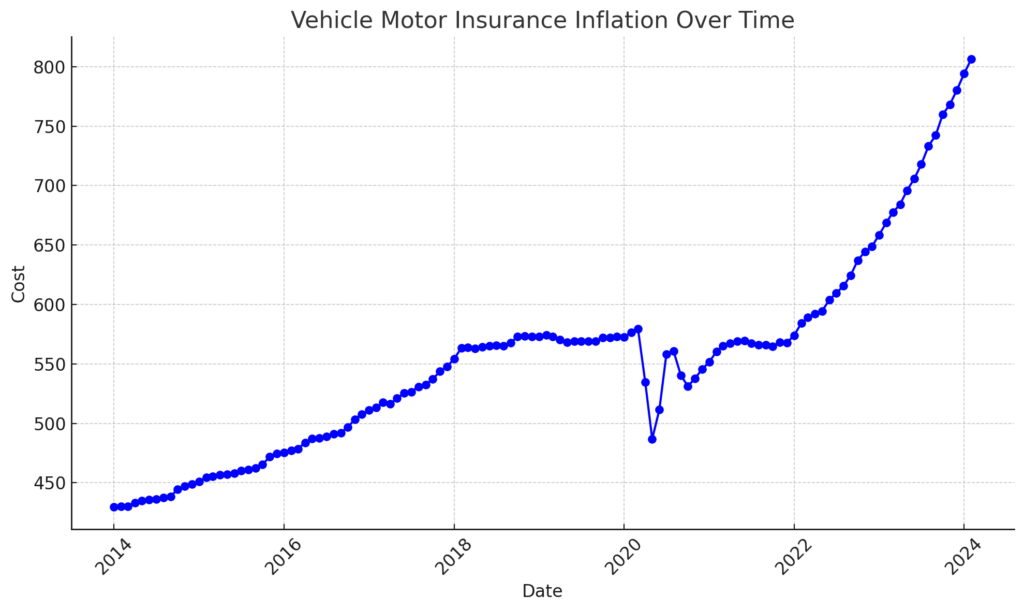

The big news today was the release of the Consumer Price Index for February 2024. You can read the full report here and look at some charts here. But you will have to dig a little bit to get the eye popping data of motor vehicle insurance here. I copied the data and asked AI to create a chart that’s a little bit better than the one at the link.

Auto insurance cost was growing steadily at a fairly even pace and it did so to adjust for the ever growing cost of cars with new bells and whistles but after COVID, insurance cost has gone haywire.

Cause and Effect

While cars cost more there is more to the problem than new/better features. First, there are still supply chain problems happening. The largest manufacturer of auto parts, China, suffered supply chain disruptions and many firms decided they didn’t want to have all their eggs in one manufacturing basket so they started diversifying where auto parts are manufactured – this added cost.

We also have unemployment at 3.9% which is the lowest level in a long time, this means that labor is more expensive today than it was 10 years ago for a variety of reasons. We also have millions of boomers that started retiring around 2011 and that retirement flow hasn’t stopped or slowed down. We will continue to have a tight labor market for at least another decade.

If you are an insurance company you are faced with high repair labor costs, high cost of replacement parts, and high cost of replacing an ever more expensive vehicle. The insurance company won’t eat or absorb all of those costs so they will simply pass those on to the consumers.

What To Do

#1 Reconsider if you really need a car. I personally work from home and don’t really need a car so I share one with my wife. She drives to work everyday and if I need the car for something, I will take her to work and do my thing then pick her up.

#2 – Consider using Uber/Lyft. This boils down to a math equation, find out how much a ride sharing service would cost to take you and return you. I did this for my wife and I BEFORE I had a remote work job and we discovered that it was cheaper for her to take a $10 Uber every day to/from work/home than to make a car payment, pay for insurance, maintenance, fuel, and other costs.

#3 – Consider changing your insurance coverage. Instead of full coverage for a vehicle that is 10+ years or older, it may be better to simply carry liability. The risk here is if your car is totaled, you may not be able to afford a new one given how crazy auto prices are now.

#4 – Consider car pooling. Ask your employer if they have a car pooling service that can be shared by employees. If not, consider getting a group together and asking the company to offer this as a benefit.

#5 – Consider your lifestyle choices. Far too many people pick impractical locations to live leaving their primary income location so far away that a car is needed to go to/from the location.

#6 – Consider a remote job. While not as available now as they were during the post pandemic time frame, there are still jobs that offer remote work.

Ultimately, if insurance costs keep escalating at their current rate, people will be forced to pick from #1-#6 above or perhaps all of them. The best thing to do NOW is to have a plan in place so that you’re prepared for the inevitable insurance crisis that seems to be coming.

2 thoughts on “What To Do About High Insurance Inflation?”

Comments are closed.