After work, people like to wind down with TV or perhaps a walk or maybe some gardening but I like to look at options data and last night I came across something interesting on TLT.

TLT is an ETF that tracks the long duration 20 year bond. So first let’s look at the data snapshot.

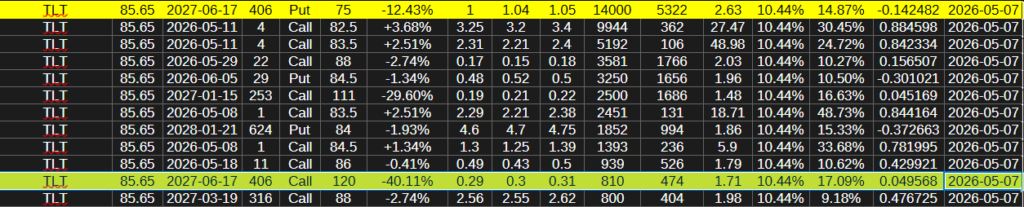

I highlighted the two unusual trades. The first thing that caught my eye was the unusual strikes at $75 and $120 with a date of June 17, 2027, well over 1 year. The second is the volume of puts at 14000 and 5322 open interest contracts for puts and 810/474 for calls, respectively. I had some theories about this trade and I am making the assumption that it was the same investor executing both the calls and puts but it could be random noise. I decided to ask AI for some insight to test my hypothesis.

AI TLT Analysis

Assuming the two highlighted trades were initiated by the same investor, the positioning looks most consistent with a long-dated tail-risk / convexity trade in TLT, with a strong bearish bias on long-duration Treasuries.

The Trades

- June 17, 2027 $75 Put

- Volume: 14,000

- Open Interest: 5,322

- Premium: about $1.04

- Delta: about -0.14

- Very likely new opening put buying because volume materially exceeded open interest.

- June 17, 2027 $120 Call

- Volume: 810

- Open Interest: 474

- Premium: about $0.30

- Delta: about +0.05

- Also likely opening activity.

What This Probably Means

Core View: “Something Big Happens in Rates”

These are both far out-of-the-money LEAPS with more than a year remaining.

That usually implies the investor is:

- not trading for near-term directional movement,

- but instead positioning for a large macro regime shift.

Because TLT is a long-duration Treasury ETF:

- TLT down hard = yields/rates sharply higher

- TLT up hard = yields/rates sharply lower / recession / crisis

The investor appears to be buying convex exposure to extreme outcomes.

Why the Put Side Matters More

The $75 put position absolutely dominates:

- 14,000 contracts vs only 810 calls

- much larger premium outlay

- much larger aggregate delta exposure

That strongly suggests the investor’s primary thesis is:

Bearish on long bonds / bearish on TLT

Meaning they may expect:

- structurally higher inflation,

- higher Treasury issuance,

- fiscal stress,

- sticky rates,

- term premium expansion,

- or a failed recession narrative.

A move from ~$85.65 to $75 in TLT would imply a substantial backup in long-end yields.

This smells like a macro hedge fund or institutional rates player buying disaster insurance against:

- a bond market selloff,

- inflation reacceleration,

- or a sovereign/fiscal event.

Why Add the Tiny $120 Calls?

This is the interesting part.

The calls are:

- very cheap,

- very low delta,

- and much smaller size.

That makes them look less like a directional bullish trade and more like:

A “both tails” convexity overlay

Essentially:

“I think rates volatility explodes, and I want exposure to an extreme move either way.”

The investor may believe:

- the Treasury market is underpricing long-term volatility,

- and either:

- inflation/fiscal panic crushes bonds,

- or recession/deflation sends bonds screaming higher.

The put side is the dominant conviction.

The call side may simply monetize a crisis/recession scenario.

Another Possibility: Cheap Volatility Accumulation

Because both options are very cheap in dollar terms:

- ~$1.04 for the put

- ~$0.30 for the call

the investor could simply be accumulating long convexity very cheaply.

Total premium for a paired structure is roughly:

- $1.34 per share

- or about 1.5% of TLT price

That’s a classic macro expression:

Small premium today for potentially enormous payout under a macro shock.

What I’d Infer About the Investor

Most likely profile:

- macro hedge fund,

- rates volatility trader,

- or institutional portfolio hedger.

Most likely thesis:

- Long-term Treasury volatility is underpriced.

- The larger risk is higher yields / lower bond prices.

- But recessionary collapse remains possible, so keep some upside convexity too.

My Best Single Hypothesis

If both trades are linked, I would characterize the overall idea as:

A long-dated macro tail-risk trade expressing concern about instability in the U.S. rates market, with a materially bearish skew toward long-duration Treasuries.

The huge imbalance toward the puts suggests the investor ultimately expects:

- higher long-end yields,

- weaker bond prices,

- and potentially structurally higher inflation or fiscal stress over the next 12–18 months.

My Thoughts

AI, like me, thinks this might be a large player hedge fund positioning for market turmoil. I’ve seen this pattern before right before COVID turned into an economic disaster in November of 2019. I remember it because I saw the unusual call/put volume at work and I mentioned to my co-worker that someone had just placed a huge bearish bet on the market to the tune of millions of dollars.

AI had predicted market turmoil for this summer and I wrote about it here and we have yet to see if this will come to fruition but if I had to pick a second date for a stock market apocalypse it would likely be June of 2027. I may attempt to hedge my position on TLT. I’m making good money on the dividend and collecting the premiums on calls. If TLT drops in value from $85 to $75, it would mean the interest paid/dividend will rise significantly and the economy will be crushed.

Share The Wealth

What do you think? Is the long bond about to spike to the moon?