The chip makers like NVDIA and TSM seem to be running out of steam. They are still growing but the rage is now all on RAM and Storage with companies like Micron growing 400% in months. This got me thinking about the whole AI ecosystem and what might come next. Rather than spend hours of time researching, I decided to ask AI for its thoughts.

AI created this infographic and more detail is below if you’re interested. In some ways, I was way ahead of the power but because of different reasons, I bought into Generac because I thought the Iran-oil crisis would cause shortages of power eventually so I entered into a position. It did not occur to me that AI might gobble up all the power generators. A win either way!

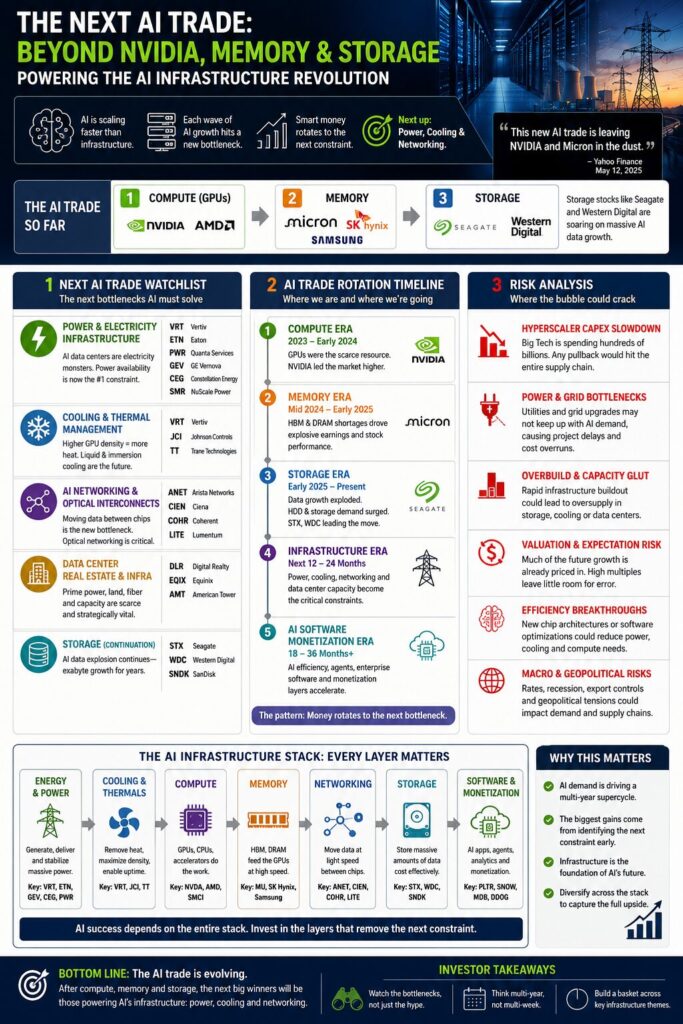

AI Research

1. Power & Electricity Infrastructure (Most Likely Next Mega Trade)

AI datacenters are becoming electricity monsters.

Training was already power-hungry, but inference at global scale may require vastly more continuous power. The industry is now realizing:

- GPUs are useless without power availability

- Utilities cannot upgrade grids fast enough

- Datacenter operators are desperate for reliable electricity

That shifts attention toward:

- Electrical equipment

- Grid modernization

- Transformers

- Cooling systems

- Nuclear power

- Natural gas generation

Likely beneficiaries:

- VRT (cooling + power infrastructure)

- ETN

- PWR

- GEV

- SMR

- CEG

The market increasingly believes AI’s limiting factor is no longer chips — it’s energy delivery.

2. Cooling & Thermal Management

AI racks are running so hot that traditional air cooling is becoming obsolete.

That creates demand for:

- Liquid cooling

- Immersion cooling

- Heat exchangers

- Thermal materials

- Datacenter HVAC redesign

This is a “picks-and-shovels” trade similar to memory in 2024–2026.

Watch:

- VRT

- JCI

- TT

Why this matters:

Every new GPU generation increases rack density and heat output. AI scaling physically breaks old datacenter designs.

3. Optical Networking / AI Interconnects

Once GPUs became fast enough, moving data between them became the bottleneck.

Now hyperscalers are racing to improve:

- Optical transceivers

- Silicon photonics

- High-speed networking

- Co-packaged optics

This could become the “next NVIDIA” style narrative because networking scales with every AI cluster expansion.

Names to watch:

- ANET

- CIEN

- LITE

- COHR

NVIDIA itself has acknowledged networking is now strategic through InfiniBand and Spectrum-X.

4. AI Datacenter REITs & Infrastructure Land

This is more subtle but potentially huge.

AI facilities need:

- Massive power access

- Fiber connectivity

- Water access

- Physical land near grids

That benefits:

- Datacenter REITs

- Industrial infrastructure owners

- Fiber network operators

Potential beneficiaries:

- DLR

- EQIX

- AMT

This mirrors historical telecom buildouts.

5. AI Inference Efficiency Software (Longer-Term)

Once infrastructure spending peaks, investors usually rotate toward:

- software monetization

- AI efficiency

- orchestration layers

- AI agents

- enterprise AI productivity

This is probably the later phase, not the immediate next phase.

Potential leaders:

- PLTR

- SNOW

- MDB

- DDOG

My read on the sequence

The AI trade evolution has roughly looked like:

- Compute

- NVIDIA

- AMD

- Memory

- Micron

- SK Hynix

- Samsung

- Storage

- Seagate

- Western Digital

- Power + Cooling + Networking ← likely current/next phase

- AI monetization software ← later-cycle phase

The key pattern:

Each wave shifts toward the next constraint in the AI stack.

Right now, the biggest constraints increasingly appear to be:

- electricity,

- heat,

- networking bandwidth,

- and physical datacenter capacity.

That’s why many institutional investors are now studying utilities and industrials almost as closely as semiconductors.

1. Watchlist

Core next-wave names: VRT, ETN, GEV, PWR, ANET, CIEN, COHR, LITE, CEG, DLR, EQIX. Storage continuation: STX, WDC, SNDK.

2. Rotation timeline

Compute → memory → storage → power/cooling/networking → AI software monetization. The power angle is especially strong because AI data centers are pushing U.S. electricity demand to record highs and stressing grid planning.

3. Bubble-crack risks

Watch for hyperscaler capex cuts, grid delays, overcapacity, valuation compression, and efficiency breakthroughs that reduce demand for hardware. Big Tech AI capex is enormous, but that also means free cash flow and investor patience become key constraints.

My Thoughts

I am not a big fan of investing individual stocks unless there is a compelling reason so I ended up investing in these three “AI” ETFs and most are up 16% or higher since I started: AIQ, DTCR, PAVE.

- AIQ holds chip makers, memory makers, network component makers

- DTCR holds REITs and related infrastructure for data centers

- PAVE holds the heavy machinery needed to build data centers

I also bought XLI a while back on the premise it does well during recessions but it is doing very well now on the AI boom. But my biggest gain was buying EWY during the Iran war panic. I bought more as it dipped and sold calls. I may roll them and buy puts to lock in gains.

Share The Wealth

Are you cashing in on the AI trade or did you get left behind?